Market Update: Market fears fading

Matt Davies, Trump debate is a dog’s dinner, 12 September 2024

Market fears fading

Continued resilience of the US economy calmed markets, but nervousness remains if the big central banks get their PR messaging around further interest rate cuts wrong.

Budget and growth gloom make UK rate cut a certainty

Labour in full ‘blame the Tories’ mode as dire public finances, and a sluggish economy, create a clear path for the Bank of England.

How China trades

We lift the lid on the factory of the global economy with import tariffs hurting exports, and weak domestic demand rolling on.

Market fears fading

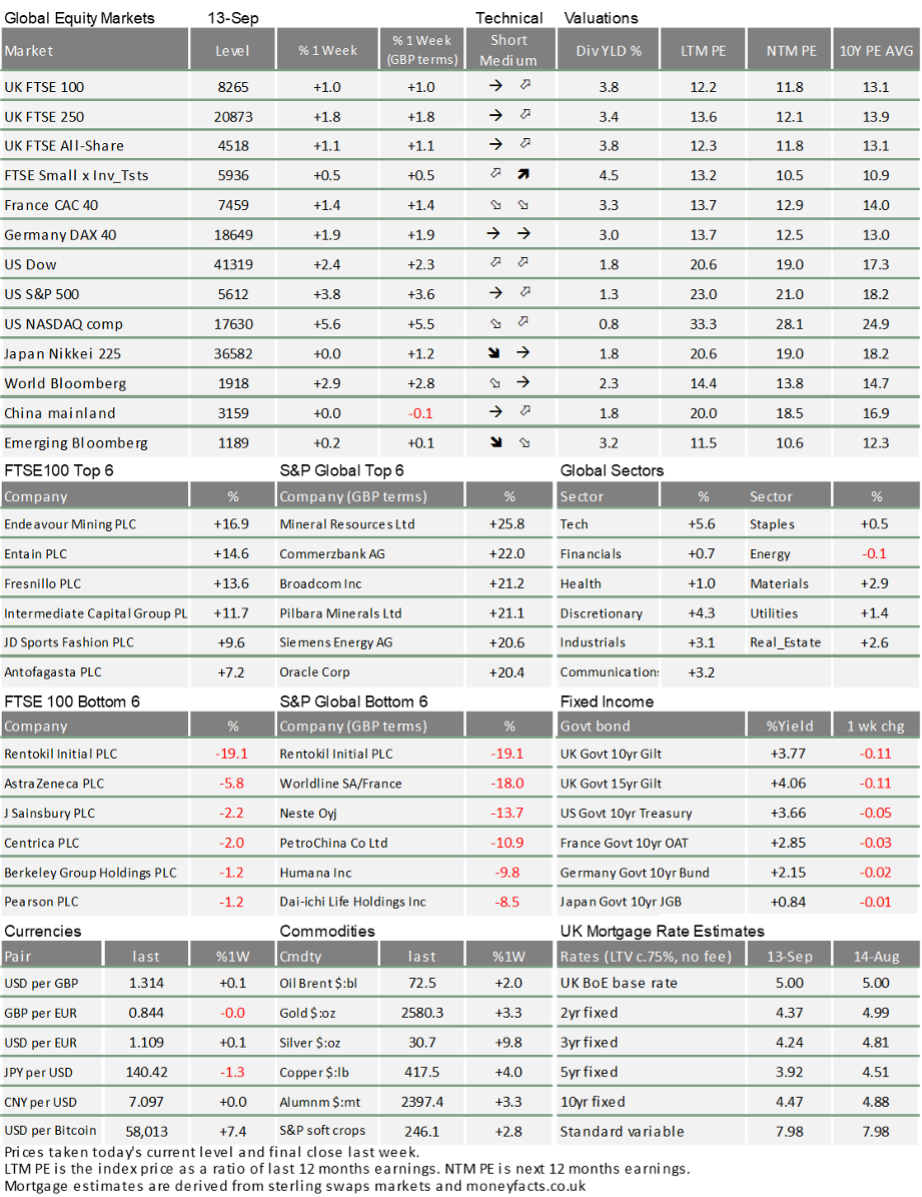

Capital markets picked themselves up last week. Global stocks are up, recovering well from a tough start to September. At the time of writing, not all of the week before last’s losses have been recovered, but markets seem to breathe a sigh of relief. This was particularly felt in the US, where stocks gained every day of the week at a remarkably consistent pace. We said before that the early September sell-off felt a little like the one that began at the height of summer – more about nerves than underlying outlook. Last week’s steady recovery felt a little like what we saw for the rest of August, too. The August one eventually ran hot – probably a factor behind the week before last’s sell-off – but there thankfully are no signs of a repeat yet.

The ECB cut rates but sounded hawkish.

The European Central Bank (ECB) cut interest rates for the second time last week by 25 basis points (0.25%) – the same as in June and in line with market expectations, taking Eurozone benchmark rates down to 3.5%. But ECB President Christine Lagarde downplayed the likelihood of another cut in October and noted: “A declining path is not pre-determined, … Neither in terms of sequence nor in terms of volume.” Markets considered this a surprisingly hawkish (preferring higher rates) message and the implied rate curve – mapping out where bond traders expect Eurozone rates to be over the next year – flattened slightly.

We should not overinterpret Lagarde’s hawkishness; she said further cuts were likely, just not guaranteed. But there are clearly those inside and out of the ECB that think cutting too much too soon would be a mistake. On Wednesday, a former member of the ECB’s supervisory board wrote a Financial Times opinion piece arguing that the “ECB has no room to cut rates”. They noted the stickiness of services inflation (up to 4.2% in August from 4% in July) and the fact that the ECB’s 3.5% interest rate is already nearly 2 percentage points below US rates.

The argument is that the ECB must follow its own path and not the one set by the US Federal Reserve – a line ECB policymakers have emphasised. But this misses the point somewhat. Markets expected a steep decline in Eurozone rates not because of what the Fed is doing, but because Europe’s economy is clearly in need of a boost.

Former ECB president Mario Draghi stressed as much last week in his report to the European Commission. He called for a “new industrial strategy” and significant investment, to avoid European growth falling further behind the US and China. The structural weaknesses he notes are not the ECB’s fault, nor within the ECB’s power to truly resolve – but they arguably call for a more dovish approach than the bank is prepared to take.

US markets in a better mood.

By contrast, the Fed’s dovishness has set the scene nicely for US markets. The S&P 500 closed trading higher every day last week, and was buoyed by August’s inflation data. Headline inflation was 2.5%, below the expected 2.6%, but core prices (excluding volatile elements like food and energy) were higher than expected month-on-month. This suggests that disinflation is coming from input prices (much of it from China) while domestic demand remains strong.

Interestingly, this kind of scenario probably would have unnerved markets a few months ago – suggesting persistent inflation and delayed rate cuts. But after a short sharp intraday blip, investors thought it was good news. There have been fears recently that the US economy might be slowing too much, so markets now seem happy about signs of resilience. This goes hand in hand with a general sense that previous market fears are dissipating. Nvidia’s shares showed a very strong recovery last week – up more than 10% from last Friday at the time of writing – after the chipmaker’s CEO reassured investors of continued microchip demand.

Stocks were not moved in either direction by the political highlight of the week, the US presidential debate – though Bitcoin weakened, which analysts have taken to be a bearish sign for Donald Trump’s chances, given his outspoken support for cryptocurrencies. The consensus view is that Vice President Kamala Harris came off better on the night, but probably not by enough to make her the clear favourite. This election has potentially enormous impacts for global assets, but there is too much uncertainty in this close race for markets to make a call on what those impacts will ultimately be.

All eyes on the Fed.

Attention now turns to the Fed’s meeting this week, where markets are fully expecting an interest rate cut of 25 basis points. Expectations of a 50 point cut have come down in response to Wednesday’s solid inflation figures, and it could even be a negative surprise for investors if the Fed did opt for a bigger cut. Markets want lower rates, but the economic data suggests 25 points is appropriate – so anything more could be interpreted as the Fed lacking confidence in the US economy.

Financial media frequently discusses how big particular cuts might be, but over the long-term they have relatively minor impacts. The trajectory and pace of interest rate changes are more important – and everyone agrees that the Fed will keep cutting rates. The central bank has been as clear as it can be that it wants to make policy more accommodative, and this will support both bonds and equities.

The Fed’s supportive stance still perplexes some, considering the US’ continued economic strength and, hence, lack of rate cut urgency compared to Europe. But as the Fed has communicated, inflation and (particularly) employment are at an inflection point – where things could quickly get worse if left unchecked. The problems at car finance firm Ally Financial – whose shares sunk 16% on Tuesday after its CEO warned of its borrowers struggling – highlight that there are pockets of the US economy where high interest rates are taking a toll. That is why the Fed will cut this week, and why its commentary will be crucial for how US and global markets fare. This also brings the potential of further market volatility, should officials decide to deviate from consensus expectations.

This week’s writers from Tatton Investment Management:

Lothar Mentel

Chief Investment Officer

Jim Kean

Chief Economist

Astrid Schilo

Chief Investment Strategist

Isaac Kean

Investment Writer

Important Information:

This material has been written by Tatton and is for information purposes only and must not be considered as financial advice. We always recommend that you seek financial advice before making any financial decisions. The value of your investments can go down as well as up and you may get back less than you originally invested.

Reproduced from the Tatton Weekly with the kind permission of our investment partners Tatton Investment Management

Who are Vizion Wealth?

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

Our approach to financial planning is simple, our clients are our number one priority and we ensure all our advice, strategies and services are tailored to the specific individual to best meet their longer term financial goals and aspirations. We understand that everyone is unique. We understand that wealth means different things to different people and each client will require a different strategy to build wealth, use and enjoy it during their lifetimes and to protect it for family and loved ones in the future.

All of us at Vizion Wealth are committed to our client’s financial success and would like to have an opportunity to review your individual wealth goals. To find out more, get in touch with us – we very much look forward to hearing from you.

The information contained in this article is intended solely for information purposes only and does not constitute advice. While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, Vizion Wealth is not responsible for any errors or omissions. In no event will Vizion Wealth be liable to the reader or anyone else for any decision made or action taken in reliance on the information provided in this article.